Last updated: July 7, 2026 · Data reviewed quarterly

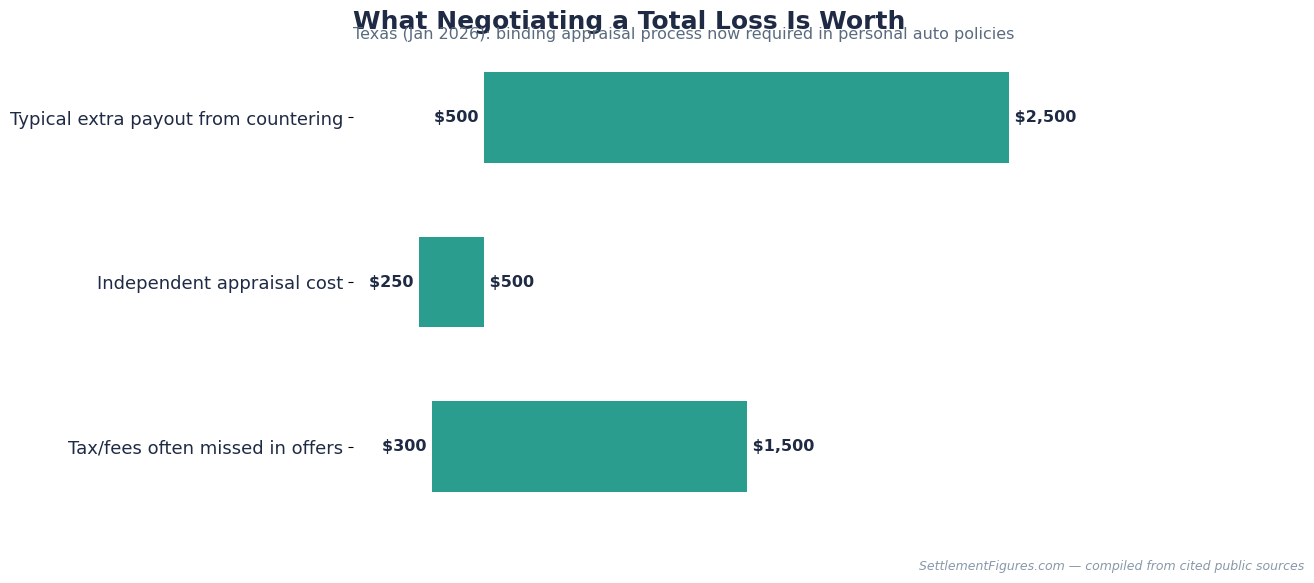

When your car is totaled, the insurer’s first offer comes from a third-party valuation report built to find the cheapest “comparables” available. Negotiating that number with real evidence adds $500 to $2,500 on average — for one afternoon of documented pushback.

How they get their number (ACV)

Actual Cash Value = what your exact car would sell for locally the day before the crash. Insurers buy valuations from data vendors whose reports lean on comps that are often base trims, higher mileage, or hundreds of miles away with “market adjustments.” You are owed that report — demand the full comps list; that is where the discount hides.

The negotiation, step by step

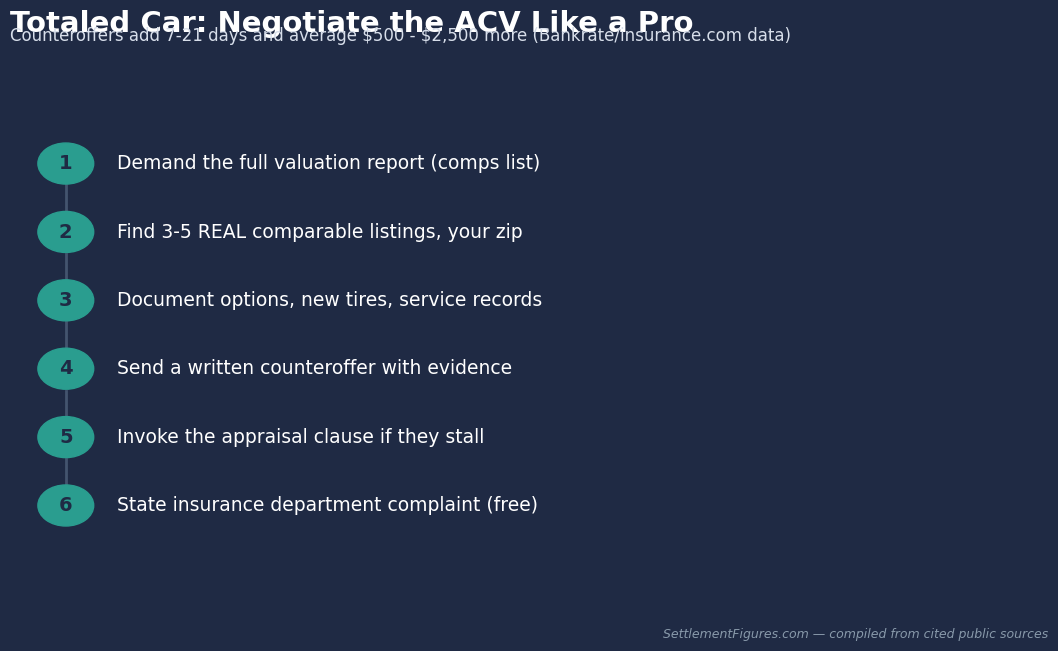

1) Get the valuation report and read every comp. 2) Pull 3-5 REAL listings for your year/trim/mileage in your zip radius (screenshots with dates). 3) Document what the report missed: option packages, new tires (receipts), service records, pre-crash photos. 4) Send a written counter with evidence and a specific number. 5) If they stall, invoke the appraisal clause in your policy — each side hires an appraiser and disagreements go to an umpire; Texas even made a binding appraisal process mandatory for personal auto policies effective January 1, 2026. 6) Stonewalling → state complaint path.

The line items almost everyone forgets

| Item | Typical value | Note |

|---|---|---|

| Sales tax on the ACV | 5 – 10% of payout | Owed in most states — verify yours |

| Title & registration fees | $50 – $500 | Part of replacing the vehicle |

| Recent tires/brakes/battery | $200 – $1,200 | With receipts, adjusters add them |

| Options the report missed | $300 – $2,000 | Tow package, premium audio, AWD trim |

| Rental during the process | Policy-dependent | Do not return it early under pressure |

Keep it or let it go?

You can usually keep a totaled car minus salvage value — sensible for cosmetic totals on older cars, but the salvage/rebuilt title cuts future resale 20-40% and complicates insurance. And if the payout dispute is really about the crash being minor, check whether it should have been a repair with a diminished value claim instead.

Free official help & resources

- Baseline your car’s value: KBB · JD Power/NADA guides

- State thresholds & your rights: insurance department via NAIC

- Negotiation walk-throughs: Bankrate · Insurance.com

- Loan bigger than payout? That is gap insurance — check your financing docs

FAQ

The offer is less than my loan balance.

The insurer owes market value, not your loan. Gap coverage pays the difference — check before panicking.

How long do I have to accept?

Offers rarely expire by law, but storage fees accrue on the wreck. Negotiate promptly — in writing.

They totaled it but I think it is repairable.

State thresholds (often 70-80% of ACV) force the call. Contest the repair estimate driving the ratio — or keep-and-repair via the salvage option.

☕ This research is reader-supported. No law firm pays us. If this guide saved you time or money, you can buy the research team a coffee — it keeps the data free and updated.

This article is for informational purposes only and is not legal advice. Settlement values vary significantly by case and by state. Consult a licensed attorney in your state before making decisions about your claim.