Last updated: July 7, 2026 · Data reviewed quarterly

Your repaired car is worth less than an identical never-crashed one — and in most states, the at-fault driver’s insurer owes you that difference. It is called a diminished value claim, insurers calculate it with a formula designed to lowball (17c), and knowing how it works routinely turns a $900 offer into a $3,000+ recovery.

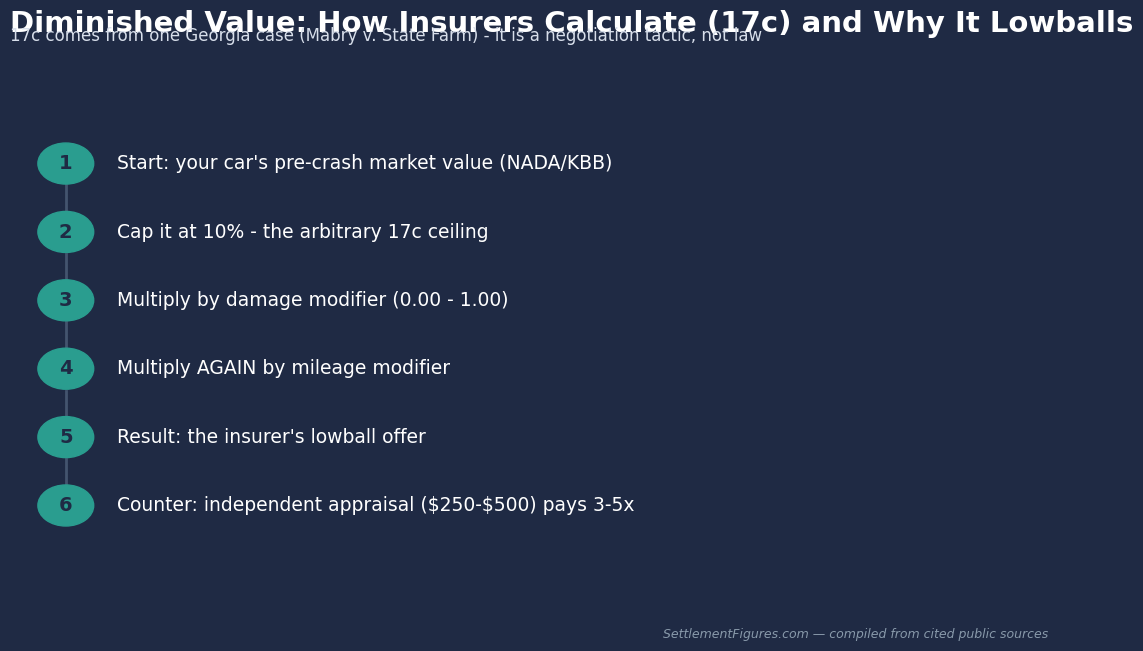

The 17c formula, exposed

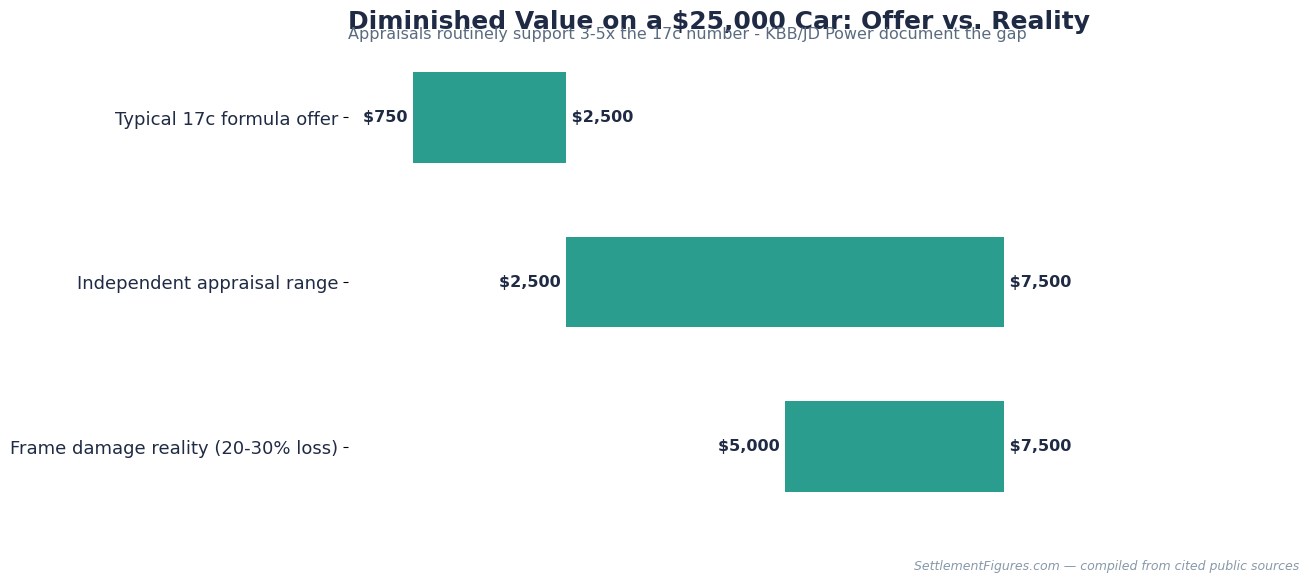

Born from a single Georgia case (Mabry v. State Farm, 2001), the 17c method starts with your car’s pre-crash market value, caps the possible loss at an arbitrary 10%, then multiplies by a damage modifier (0.00-1.00) and AGAIN by a mileage modifier. Example: $25,000 car → $2,500 cap → ×0.75 moderate damage → ×0.60 mileage → $1,125 offer — for a car that lost $4,000-$6,000 of real resale value. Every multiplication is a discount stacked on a cap with no market basis.

What your claim is actually worth

| Damage level | 17c-style offer | Market reality |

|---|---|---|

| Minor (panels, no structure) | $500 – $1,200 | $1,500 – $3,000 |

| Moderate (airbags, quarter panel) | $900 – $2,500 | $2,500 – $7,500 |

| Frame / structural damage | $1,500 – $2,500 (capped!) | 20-30% of value — $5,000+ on a $25k car |

How to actually collect

1) Claim against the AT-FAULT driver’s insurer (third-party) — first-party DV is excluded in most policies, Georgia being the famous exception. 2) Get an independent appraisal ($250-$500): appraisers document 3-5x the 17c figures using real dealer and auction data, per KBB and J.D. Power analyses. 3) Send a written demand attaching the appraisal, the CARFAX showing the reported accident, and comparable listings. 4) Refused? Same escalation as any dispute: appeal and state complaint path. Mind the deadline — DV follows property-damage statutes of limitation (2-6 years by state).

When DV is not worth chasing

Older cars (8+ years), high mileage, prior accidents on the history report, or damage under ~$2,000 usually produce DV too small to fight for. The sweet spot: vehicles under 5 years old, clean history, repair bills over $5,000 — there the diminished value often rivals the repair cost. Totaled instead of repaired? Different fight: total loss negotiation.

Free official help & resources

- Market value baselines: KBB.com · JDPower.com (both publish DV guidance)

- Vehicle history that proves the hit: your CARFAX/AutoCheck report

- Insurer refuses to engage: state insurance department via NAIC

- Small claims court: DV amounts often fit the limits — self-help via USA.gov

FAQ

The insurer says my state does not allow DV claims.

Third-party DV is recognized in the vast majority of states. Ask them to cite the statute — that sentence usually ends the bluff.

Can I claim DV if I never plan to sell?

Yes — the loss exists at the moment of the accident, not at resale. Courts value it at repair completion.

Leased car — who gets the money?

Usually the leasing company holds the right; check your lease. Some negotiate splits, since you eat the loss at turn-in inspection.

☕ This research is reader-supported. No law firm pays us. If this guide saved you time or money, you can buy the research team a coffee — it keeps the data free and updated.

This article is for informational purposes only and is not legal advice. Settlement values vary significantly by case and by state. Consult a licensed attorney in your state before making decisions about your claim.