Last updated: July 7, 2026 · Data reviewed quarterly

A denied insurance claim is an argument, not a verdict — and insurers reverse a meaningful share of denials when policyholders push back with evidence. Here is the appeal path that actually works, from the denial letter to your free state-level complaint.

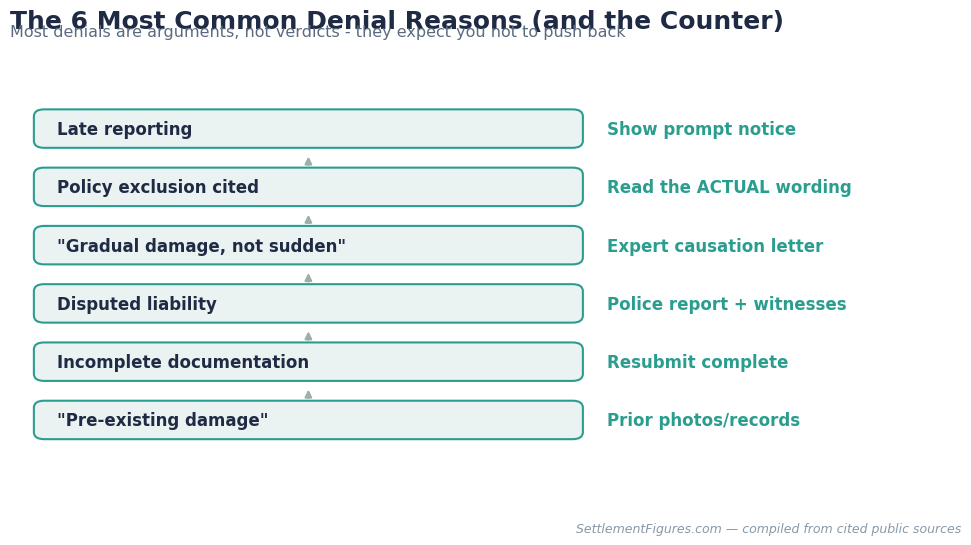

First, decode the denial

| Denial reason | The counter that works |

|---|---|

| Late reporting | Show prompt notice: call logs, emails, portal timestamps |

| Policy exclusion cited | Match the letter against the ACTUAL policy wording — exclusions get stretched |

| “Gradual damage, not sudden” | Plumber/contractor causation letter; photos with dates — the classic water damage fight… on any policy type |

| Disputed liability | Police report, witness statements, photos |

| Incomplete documentation | Resubmit complete — denials for paperwork are invitations, not endings |

| “Pre-existing damage” | Prior inspection reports, dated photos, maintenance records |

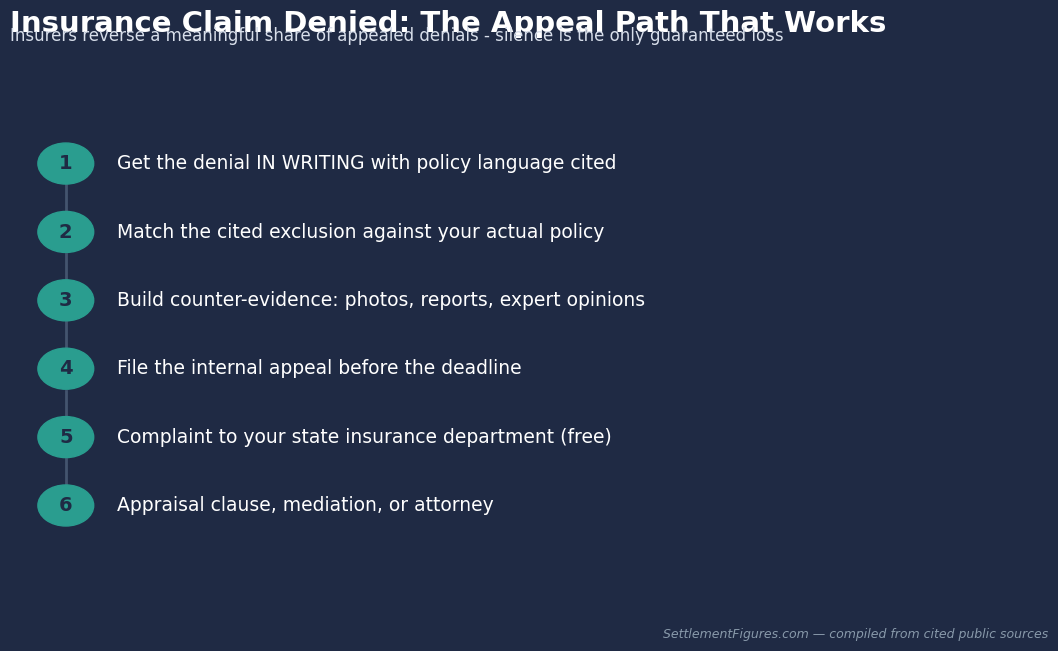

The appeal sequence (do not skip steps)

1) Demand the denial in writing with the specific policy provisions cited — insurers must provide this. 2) Read those provisions yourself; a surprising number of denials cite language that does not say what the adjuster claims. 3) Build the counter-file: photos, expert letters, receipts, comparable claims. 4) File the internal appeal within the deadline (often 30-180 days), in writing, attaching everything. 5) Escalate outside: your state insurance department accepts complaints free, and insurers answer them because regulators track patterns. 6) Still stuck? Policy appraisal clauses, mediation, or counsel — many take strong coverage cases on contingency.

The letter that changes tone

One page, certified mail: the claim number, the denial’s cited provision, your evidence list, a specific demand, a deadline (14-21 days), and one sentence noting you will file a complaint with the state insurance department if unresolved. Adjusters triage: files that look litigation-ready get reassigned to people with settlement authority.

Bad faith: when denial becomes its own claim

Insurers owe a duty of good faith. Ignoring evidence, misrepresenting policy language, slow-walking without reason, or lowballing against their own adjuster’s notes can create liability BEYOND the claim — several states allow penalty damages. Document every interaction with dates; the paper trail is the bad-faith case.

Free official help & resources

- File a state complaint (free, effective): find your insurance department via NAIC consumer resources

- Policy language help & consumer guides: III.org

- Free legal aid for coverage disputes: LSC.gov · ABA Free Legal Answers

- Health-claim denials (different rules, same spirit): HealthCare.gov appeals — healthcare.gov

FAQ

How long do appeals take?

Internal appeals: 30-60 days typically. State complaints force a written insurer response usually within 30 days — and often shake loose settlements by themselves.

Will appealing raise my premiums?

Appealing a decision does not add a claim — the claim already exists. Fear of premiums is how underpaid claims stay underpaid.

The adjuster reopened negotiation after my complaint. Coincidence?

No. Regulator statistics are one of the few metrics insurers universally manage.

☕ This research is reader-supported. No law firm pays us. If this guide saved you time or money, you can buy the research team a coffee — it keeps the data free and updated.

This article is for informational purposes only and is not legal advice. Settlement values vary significantly by case and by state. Consult a licensed attorney in your state before making decisions about your claim.